Transparent Network Technology

by Joseph Mark Haykov

April 10, 2024

Abstract

Transparent Network Technology (TNT) operates via a decentralized network of peer-to-peer nodes. These nodes, independently owned and operated, link together through the internet, forming a unified cluster. This collective entity oversees a blockchain-based banking ledger, akin to the Bitcoin blockchain general ledger, adhering to the stringent principles of double-entry bookkeeping. This method ensures the accurate maintenance of all account (or wallet) balances. Unlike systems that rely on specialized nodes—such as Bitcoin miners or Ethereum validators—for transaction validation through computationally intensive proofs, TNT employs a consensus algorithm that utilizes batch processing. This technique not only simplifies the transaction verification process but also reduces the system’s operational complexity and energy consumption.

Introduction

Before exploring the complexities of cryptocurrencies, it is crucial to first understand the diverse perspectives on the very nature of money. The Arrow-Debreu equilibrium model, a cornerstone of mathematical economics, views money primarily as a unit of account. According to this model, money serves as a universal measure for valuing goods and services, a notion that has sparked considerable debate within academic circles. This debate is thoroughly examined in scholarly works, including the notable study "A Walrasian Theory of Money and Barter." The paper argues that focusing solely on money's function in pricing overlooks its broader significance and utility. Such discussions underscore the importance of examining money's multifaceted roles to fully appreciate the implications of emerging financial technologies like cryptocurrencies.

Emerging from the late 19th century's flourishing mathematical economics field, visionaries like William Stanley Jevons, Carl Menger, and Léon Walras emphasized money's role as a medium of exchange. They hypothesized that the creation of money was a natural response to the inefficiencies of barter systems, particularly the "double coincidence of wants"—the challenge of two parties possessing mutually desired goods or services. This stance stands in stark contrast to the Arrow-Debreu model's unit of account focus as the key role of money, spotlighting a profound and ongoing debate within economic thought—a debate still lacking a universally accepted resolution.

The discourse on what constitutes money extends beyond academic debates and high-profile interactions, like the argument between Ron Paul and Ben Bernanke during congressional hearings. It deeply influences the spheres of professional investing, corporate governance, and economic scholarship, where there's significant disagreement on whether assets like gold and Bitcoin qualify as money. These vigorous debates test the boundaries of established financial theories and practices. The persistent nature of such discussions underlines the challenges in achieving a consensus on money's definition, complicating the understanding of cryptocurrencies.

The contrasting perspectives on the essence of money highlight a critical need for reevaluating traditional economic theories. However, delving into these theoretical bases is beyond the scope of our discussion on TNT, an innovative payment system poised to revolutionize cryptocurrency transactions. Consequently, we steer our examination towards concrete, observable evidence, distancing ourselves from theoretical disputes. Our objective is to clarify the practical functions of money in economic transactions. Leveraging the Federal Reserve's Economic Education resources, we achieve a comprehensive empirical understanding of money's essential roles, consciously steering clear of speculative theoretical models. According to the Federal Reserve, the institution behind the issuance of the U.S. dollar, money serves three crucial functions in the real economy:

Unit of Account: Money establishes a universal value metric, making economic transactions more straightforward by facilitating easier pricing and accounting. This function is crucial for enabling individuals and businesses to make sound financial decisions.

Medium of Exchange: Money overcomes the limitations of barter systems by acting as a widely accepted intermediary in the exchange of goods and services, which is indispensable for the seamless functioning of market economies.

Store of Value: Money provides a mechanism for saving and future planning by maintaining value over time, thereby contributing to economic stability and growth.

The fundamental roles of money, as a unit of account, a medium of exchange, and a store of value, are not only universally acknowledged in modern societies but have also been evident throughout history. No currency has ever been considered viable without successfully fulfilling these three essential and obligatory functions. The effectiveness with which a currency performs these roles is a key determinant of its acceptance and practical use within an economy. It underpins a wide range of economic activities, from daily transactions to comprehensive financial planning. This understanding is grounded in empirical evidence rather than just theoretical speculation, a point underscored by the Federal Reserve, the authority behind the issuance of the U.S. dollar.

Consider the example of a dollar in your bank account: it symbolizes a quantifiable measure of purchasing power, existing not as physical cash but as a digital entry. This balance, denoted in dollars, quantifies your purchasing power, akin to how weight is quantified in pounds or kilograms, or temperature in Celsius or Fahrenheit. Your wealth, represented digitally, serves as a unit of account in the Arrow-Debreu sense, illustrating how the modern economy relies on the dollar to assess and compare economic values. This practical example bridges the abstract monetary theories with the concrete realities of financial transactions, underscoring the indispensable and multifaceted roles of money in the seamless operation and advancement of economies across time.

Exploring money's function as a unit of account reveals one of its pivotal roles within the economy. However, money's significance extends further, serving both as a medium of exchange and a store of value. These essential functions are crucial for the efficient operation and stability of financial transactions, underscoring money's vital role in the financial system and the broader economy. A closer look shows that any form of money—whether digital units in a bank account or physical assets like gold coins—can serve as a store of value to protect wealth for future use or as a medium of exchange to facilitate immediate purchases. Yet, it cannot simultaneously fulfill both roles, highlighting a fundamental trade-off between saving and spending, a concept known as money’s exclusive dual-use.

The principle of exclusive dual-use serves as a vital link between intricate economic theories and the practicalities of everyday financial activities. It emphasizes the inherent challenge of using the same unit of money for both saving and spending, barring unethical practices like check fraud. This principle sheds light on the strategic use of money, connecting abstract economic concepts with real-world financial management. Central to grasping money's complex roles in our economy is this principle, succinctly captured by the equation U = S + E. 'U' represents money's role as a unit of account—encompassing the entire money supply. 'S' stands for its function as a store of value, including gold coins in a vault or funds in a savings account earmarked for future use. 'E' illustrates its utility as a medium of exchange, indicating the portion of the money supply in active circulation for transactions. While money consistently serves as a measure of value, at any given moment, it operates as either a store of value or a medium of exchange, but never both.

The concept of exclusive dual-use enriches our understanding of money's intricate roles in the economy, affecting everything from personal finance to national economic strategies. The Federal Reserve's M2 money supply data exemplifies this principle in real terms. Consider an M2 total of $21 trillion (U=$21 trillion), with $15 trillion in active circulation for transactions (E=15) and $6 trillion in savings (S=6), not presently used in transactions. This breakdown vividly demonstrates how distinct segments of the money supply serve different functions, based on their current usage.

M2 assets, encompassing cash, checking deposits, savings accounts, and other forms of near money, are defined by their immediate accessibility on demand, positioning them as a crucial component of the money supply available for use as a medium of exchange. This categorization highlights the inherent liquidity of M2 assets, making them indistinguishable in their function as money, regardless of the account type. They are designed to be rapidly deployed for various economic activities, including facilitating transactions, purchasing goods and services, or fulfilling tax obligations.

The liquidity inherent in M2 assets becomes particularly crucial in economic scenarios characterized by low interest rates and modest inflation. In these contexts, the ability to swiftly access and utilize funds offers a significant edge. This liquidity ensures economic agility and responsiveness, empowering individuals and businesses to adeptly maneuver through financial environments.

In contrast, the process of converting bonds or other less liquid investments into spendable M2 assets often entails additional steps, which may expose individuals to market volatility and potential delays in accessing their funds. This situation highlights the substantial liquidity advantage provided by M2 assets, including savings accounts. Like checking deposits, these assets are primed for immediate deployment in various economic undertakings, reinforcing their essential role in sustaining the dynamism of economic activities.

The fluid nature of money, consistently acting as a unit of account while fluidly oscillating between a store of value and a medium of exchange, embodies the principle of exclusive dual-use. This principle underscores the significant role of the Federal Reserve's monetary policy in shaping the economic landscape. By adjusting bond yields, the Fed directly influences the money supply, affecting liquidity, interest rates, and the broader economic dynamics.

This interplay is not just a practical demonstration of money's functions as reported by the Federal Reserve but also resonates deeply with the theoretical foundations laid out by pioneering economists of the late 19th century, such as Jevons, Menger, and Walras, as well as the comprehensive Arrow-Debreu framework. The U = S + E equation, therefore, serves as a bridge, connecting these historic economic insights with contemporary monetary policy and its effects on the economy, illustrating a comprehensive view of money's pivotal roles.

The casino chip in Las Vegas offers an intriguing exploration into the unique role of money within a specific ecosystem. Outside the broader economy, the casino chip isn't recognized as conventional money. Yet, within the casino's domain, it assumes a multifaceted role. For gamblers, it serves as a store of value, securing their financial engagement in various games. Simultaneously, it operates as an exact unit of account, meticulously documenting players' wins and losses, making the intangible tangibly measurable.

Despite these roles, the chip's function as a medium of exchange is somewhat restricted to the casino's environment. Its primary use is for transactions within the casino, such as game participation or perhaps tipping services, rather than for external economic transactions. This limitation underscores the chip's specialized utility, highlighting a fascinating instance of how money's functions can be contextually adapted and constrained within particular settings.

The contrasting scenarios between the casino chip and the Venezuelan Bolivar illuminate the diverse roles money can play under varying economic conditions. The casino chip, within its niche environment, effectively serves as both a store of value and a unit of account, safeguarding gamblers' stakes and tracking their transactions with precision. This specialized application starkly differs from the challenges faced by the Venezuelan Bolivar amidst severe inflation.

Inflation has critically impaired the Bolivar's function as a store of value, making it an unreliable vehicle for savings or future financial planning. Its diminished purchasing power and the volatility of the spendable money supply relegate it primarily to the role of a medium of exchange, used for immediate transactions. However, its effectiveness as a unit of account is severely compromised by the economic instability, rendering it a poor measure for financial decision-making.

This contrast highlights the profound influence of economic stability on how money functions within an economy. The casino chip, operating in a highly regulated environment, maintains its roles effectively, whereas the Venezuelan Bolivar, amidst economic disarray, struggles to uphold its traditional monetary purposes. This situation illustrates the paramount importance of stability in ensuring that money can perform its essential functions.

In countries experiencing significant economic fluctuations, such as Venezuela, Argentina, Russia, Ukraine, and others facing similar fiscal uncertainties, the native fiat currencies often serve merely as mediums of exchange. This phenomenon aligns with the Gresham-Copernicus law, which posits that "bad money drives out good." In these contexts, "bad" local fiat currency is typically used for transactions, while "good" money—manifested in assets like dollars, euros, gold, or Bitcoin—assumes the roles of a store of value and a unit of account. Consequently, "real" prices within these economies are often quoted and assessed in more stable currencies or assets, reflecting a strategic adaptation to preserve value and facilitate economic calculation amid instability. This dynamic underscores the critical role of economic stability in determining the functional efficacy of money within any given economy.

Under the Bretton Woods system, the role of gold in the United States was carefully defined, encapsulating its significance within the global financial structure. It functioned as a unit of account, setting the standard against which all currencies, including the US dollar, were valued. Additionally, gold was recognized as a pivotal store of value, a status highlighted by French President Charles de Gaulle's significant action to repatriate gold in the late 1960s. However, despite its critical economic roles, gold was not utilized as a medium of exchange in the US economy. The legal framework of the time strictly prohibited the possession of gold coins, deeming it a criminal act punishable by up to ten years in prison. This prohibition, spanning from the confiscation of gold in 1933 to its re-legalization in 1974, mirrors the intricate interplay between monetary policy, legal stipulations, and gold's inherent value, underscoring the multifaceted nature of gold within the economic and legal domains.

In the global economic arena, the US dollar stands as a paragon of a currency that masterfully performs the three fundamental roles of money, aligning with its significant economic position. It acts as a unit of account, providing a consistent benchmark for valuing financial transactions worldwide. As a medium of exchange, the dollar streamlines international trade, offering efficiency and seamlessness crucial for the fluidity of global commerce. Furthermore, its role as a store of value ensures the preservation of purchasing power over time, a key attribute for both investors and savers.

The global trust and acceptance of the US dollar highlight its indispensable role in international finance and trade. Its proficiency in fulfilling these monetary roles not only bolsters the US economy but also establishes the dollar as the currency of choice for international transactions. This leading status in global dealings underscores the dollar's unparalleled position in the financial world.

These real-world applications of money underscore the "U=S+E" equation's relevance in depicting the practical uses and functions of money, demonstrating how a currency's roles are shaped by its stability and the particular contexts in which it operates. The US dollar's adeptness in these roles showcases its adaptability and robustness, highlighting its crucial role in ensuring the global financial system's smooth functioning.

Unraveling Money's New Era: The Shift from Tangible to Digital

In today's economy, a significant portion of money exists in digital form, recorded within financial systems as bank money. This digital currency serves as a unit of account for both saving and spending, following the U=S+E equation. Bank accounts, where these funds are held, form the cornerstone of nearly all financial transactions and savings. These funds, shown as account balances, are represented by numerical values in the financial institutions' ledgers. The value of bank money stems from its dual capability to facilitate easy payment transactions and act as a reliable store of value when not in circulation. Its widespread acceptance is due to its dependability and convenience, effectively meeting the three fundamental roles of money: as a medium of exchange, a store of value, and a unit of account, as dictated by the U=S+E equation.

Some argue that cryptocurrencies represent a profound shift in our understanding and use of money. However, all forms of currency, including digital ones like Bitcoin, conform to the U=S+E equation, a universal formula that captures the essence of money, whether it be in the form of tangible coins, tally sticks, paper bills, or digital bank entries. Throughout history, money has evolved, taking various forms such as gold coins, $20 bills, or bank money, which exists merely as numerical values in digital ledgers. Seen in this light, cryptocurrencies introduce no fundamentally new concept; they act as units of account similar to bank money, with their transactions rigorously recorded on a blockchain ledger. The depiction of Bitcoin as a tangible coin featuring a "B" and a dollar sign misleadingly suggests a physicality that doesn't exist, blurring the fact that Bitcoin and bank balances are fundamentally alike. This imagery falsely implies cryptocurrencies operate like physical coins when in reality, they parallel bank funds, where transactions bear no resemblance to the physical exchange of cash.

Grasping the distinction between digital and physical forms of money is vital as we delve into an ever-more digital financial environment, underscored by the emergence of cryptocurrencies as alternative mediums for value exchange and storage. While they might seem novel, cryptocurrencies essentially serve as a digital version of bank money. The primary distinction arises in the way their ledgers are managed; traditional bank money is documented in ledgers overseen by centralized financial institutions like JP Morgan, whereas cryptocurrencies rely on a decentralized ledger system operated by a peer-to-peer network. This shift to decentralization underscores a key vulnerability in traditional banking: intermediaries, such as JP Morgan, can fail, introducing significant counterparty risk. This risk—that the collapse of a bank could lead to a loss of wealth—is precisely what cryptocurrencies aim to address. By eliminating the middleman in ledger maintenance, cryptocurrencies seek to reduce this risk, offering a streamlined approach to managing digital transactions.

Using bank money instead of physical gold coins involves a complicated process based on the double-entry bookkeeping system. This method, which is crucial for maintaining financial records, is widely used by banks, corporations, and even within the Bitcoin blockchain. Originating from the work of Luca Pacioli in 1494, double-entry bookkeeping organizes transactions into debits and credits. This system underscores the importance of understanding the fundamental characteristics of money as technological advancements continue. The efficient financial practices observed in 16th-century Venice demonstrate that effective financial systems can function without centralization or the need for contemporary computing database technologies, providing a historical example of successful monetary management.

Traditional financial institutions excel in ledger management, meticulously recording and reconciling debits and credits to prevent account balances from becoming negative. This rigorous management acts as a defense against what is termed in computing as "double spending." Achieving such precision involves batch processing, where transactions are accumulated over the day and processed collectively, typically overnight. This approach allows for the detailed verification and reconciliation of account balances in a method that, while centralized within each institution, mirrors a decentralized operation across a bank's various branches. It maintains the integrity and security of financial transactions through careful scrutiny, ensuring that each branch has consistent and accurate information regarding all payment requests associated with an account. This meticulous process fosters uniformity and trust across the financial institution's network, guaranteeing that all branches reflect the same account status, thereby upholding the network's reliability and security.

Integrating traditional banking practices with digital currencies presents a practical solution to the intricacies of decentralized transactions. This hybrid approach merges blockchain technology with the proven principles and methods of traditional banking, utilizing the best of both worlds to enhance the management of digital currencies. This convergence not only deepens our understanding of bank money's operations but also paves the way for innovation and greater stability within the financial sector. By combining the strengths of traditional and digital finance, we can foster a more cohesive and secure financial landscape, one that is well-equipped to navigate the ongoing technological evolution.

Designing the TNT-Bank Peer-to-Peer Payment System: Synchronizing for Integrity

In the swiftly evolving world of financial technology, Trust Network Technology (TNT) emerges as a pioneering force with its peer-to-peer, node-based Layer 1 payment system. This state-of-the-art infrastructure achieves a level of synchrony and precision comparable to a meticulously coordinated symphony orchestra, made possible by recent technological advancements that streamline such complex coordination. By incorporating the Network Time Protocol (NTP) with atomic clock servers, TNT empowers any peer-to-peer network to guarantee exceptional real-time synchronization throughout its node network, attaining millisecond precision in relation to GMT. At its inception, the TNT Bank software establishes a realistic benchmark for real-time synchronization, mandating that each node synchronizes within one second of GMT. This requirement, readily attainable, sets the stage for conducting financial transactions with unmatched accuracy and reliability.

The one-second precision requirement, although modest and easily attainable by today's internet servers, plays a pivotal role in safeguarding the integrity and reliability of the TNT-Bank system. This standard introduces a structured rhythm to transaction processing that echoes traditional banking practices, where transactions are accumulated throughout the day and batch-processed after hours. By mandating that all nodes pause for three seconds after a predetermined 'closing time'—potentially occurring every minute—the system ensures comprehensive synchronization across the network, even accounting for the possibility of one-second discrepancies in the nodes' clocks. This precaution prevents any node from processing and receiving payments simultaneously, thereby mitigating the risk of double-spending and enhancing overall network uniformity. Such precise timing regulation underscores TNT-Bank's dedication to fostering a secure, efficient, and decentralized transaction environment, marrying the reliability of traditional banking methods with the innovation of contemporary financial technology.

The TNT-Bank system's design distinctly separates tasks related to transaction acceptance and processing through temporal segmentation, affording each node ample opportunity to verify and implement payment directives. This approach draws inspiration from the conventional banking model, wherein banking operations are paused overnight to reconcile the day's collected checks. Diverging from traditional consensus models like proof-of-work or proof-of-stake, TNT-Bank's unique method leverages time synchronization as a novel consensus-building strategy, marking a departure towards efficiency and enhanced security. This strategy aims to set a new benchmark for consensus mechanisms in the realm of digital currencies. Through temporal division, the system ensures thorough verification and processing of transactions, upholding the TNT-Bank system's integrity and dependability, while accelerating transaction speeds and minimizing fraud risks. This segmentation illustrates TNT-Bank's commitment to innovating within digital currency agreement methodologies, prioritizing both security and efficiency.

In the TNT-Bank system, a meticulously planned payment processing timetable is observed by the nodes: during odd minutes, they are set to receive payment requests without initiating processing, and during even minutes, they shift to processing these payment instructions without accepting new ones. This regimented scheduling grants each node the necessary time to independently verify and execute every payment request, culminating in the generation and broad endorsement of a verified update block. This systematic approach adeptly tackles the issue of scalability by effectively managing the flow of transactions, thereby ensuring the system's resilience and operational efficacy as the user base expands. The strategic temporal division of tasks not only elevates the efficiency of transaction processing but also bolsters the network's integrity and security. This method reflects the TNT-Bank system's innovative strategy to maintain superior performance and trustworthiness amidst the growing demands of digital finance.

The TNT-Bank system skillfully combines classic banking methods with advanced technological capabilities to oversee transactions. It rigorously ensures transaction verification and processing, adeptly countering potential obstacles such as network lags, node breakdowns, or security threats with its forward-thinking design. For example, to compromise the system, one would have to convince multiple autonomous, peer-to-peer nodes of an inaccurate time, like mistaking Wednesday for Thursday. Yet, this is highly unlikely due to the nodes' ability to independently verify the actual time—by observing simple cues like whether it's day or night. The system efficiently resolves any emerging issues during scheduled payment processing times using a collective approach and specific algorithms. This method promotes a unified problem-solving effort, highlighting the system's capacity for teamwork in addressing issues and providing a robust defense against diverse challenges.

The TNT-Bank system exemplifies resilience and adaptability, addressing real-world challenges such as scalability and implementing robust security measures against evolving threats. It stands as a pioneering force in the evolution of peer-to-peer payment systems. Its innovative architecture not only boosts operational efficiency and maintains network integrity but also establishes a new standard for integrating traditional financial principles with the agility of contemporary technological advancements. This positions the TNT-Bank system at the forefront of ushering in a new era of digital finance, signaling a significant shift in how financial transactions are managed and secured in an increasingly digital world.

Looking forward, the TNT-Bank system is poised to make a significant impact on the financial sector. With advancements focused on improving real-time synchronization—where batch processing is scheduled to happen every 3 seconds, allowing for all payments to be executed and confirmed in under 6 seconds—the system showcases its ability to quickly adapt to the changing needs of the financial landscape. Pilot projects and the exploration of innovative features highlight the strength and flexibility of the TNT-Bank architecture, which is prepared to meet and surpass upcoming challenges. The strategic approaches TNT-Bank adopts for synchronization, batch processing, and consensus-building are not only setting new operational benchmarks for peer-to-peer payment systems but also heralding the beginning of a new epoch in financial transactions. This forward-thinking model earmarks TNT-Bank as a forerunner of future financial technologies, envisioning a future where efficiency, security, and adaptability reign supreme.

Symmetry and Strategy: Unveiling Bitcoin's Game Theory and Economic Resilience

Understanding the factors behind Bitcoin's surge to a market capitalization of 1 trillion dollars by February 2024 is crucial. It's a common misconception that Bitcoin's security relies entirely on the complexity of its cryptographic hash functions and digital signatures. However, the true essence of Bitcoin's value lies in a Nash equilibrium, as established by the protocols encoded in its software. Whether these protocols were crafted intentionally or emerged serendipitously, they align with the principle of symmetric information in voluntary exchanges. This principle is not just a core element of mathematical game theory; it also constitutes a vital part of the Arrow-Debreau equilibrium model, which is foundational to mathematical economics.

In mathematical economics, it is posited that when trade is not only unfettered (this means not involuntary – excluding robbery, theft and such), but also equally (or equivalently symmetrically) informed, mutual benefit is assured. Thus, fraud becomes feasible only under conditions of asymmetric information, where discrepancies in what is known about the goods or services being traded can lead to opportunities for deceit. Consider the example of selling eggs: the freshness of the eggs is uncertain until they are opened. This difference in knowledge between what the seller is aware of and what the buyer can ascertain before completing the purchase creates a window for potential fraudulent activities, enabling sellers to falsely represent the quality of their eggs.

Despite the prevalent disparity in knowledge between sellers and buyers—a hallmark of most transactions—widespread fraud is not as common as one might assume. The dynamics of free-market trade naturally counteract potential fraud through mechanisms that have evolved to mitigate the risks tied to asymmetric information. The habit of repeat transactions, such as regularly buying groceries from the same vendor, acts as an effective deterrent against fraud. Sellers, motivated by the pursuit of continued business, tend to avoid dishonest practices, recognizing that such behavior can lead to the loss of loyal customers and, ultimately, their livelihood.

This self-regulating feature of market transactions highlights how the dynamics of repeated interactions and the value placed on reputation can navigate through the challenges of asymmetric information. While the mechanisms of the free market do mitigate fraud risks—evidenced by the prevalent asymmetric information alongside a relatively low occurrence of fraud—the digital realm presents unique challenges. Online fraud capitalizes on asymmetric information, leading to billions of dollars in losses each year, exacerbated by anonymity and the lack of physical interactions. The difficulties in physically verifying products and establishing a seller's credibility online underscore the risks associated with asymmetric information in digital transactions.

In scenarios where symmetric information is attainable, the dynamics of transactions shift significantly. Consider the example of purchasing fish, where its freshness can be directly assessed by buyers through smell. This immediate, tangible form of verification penetrates the veil of information asymmetry, making deceit about the fish's quality almost impossible, save for individuals with impaired olfactory functions. Symmetric information empowers buyers to demand transparency and trust, effectively eliminating the chance for fraud.

Similarly, in financial transactions, the capacity of a payment recipient to independently verify the authenticity of the currency—be it cash, gold coins, or another medium—plays a crucial role in fraud mitigation. This exemplifies the principle of symmetric information, where equal knowledge concerning the currency's authenticity exists between buyer and seller. Such equal footing serves as a robust deterrent to fraud, deterring potential fraudsters with the knowledge that any deceitful attempts are likely to be swiftly detected and thwarted.

Consequently, the incentive to counterfeit, such as manufacturing fake gold coins, dwindles. Dishonest practices like counterfeiting become both unprofitable, due to the costs and potential legal repercussions, and ineffective, as participants who can easily verify authenticity will quickly reject counterfeit items. This situation fosters a stable Nash equilibrium, where no participant benefits from straying from a strategy of honesty, provided that others maintain their honesty as well. This equilibrium enhances the monetary system's stability and integrity, demonstrating the profound impact of symmetric information on reducing fraud and reinforcing trust within economic systems.

The Bitcoin network exemplifies a Nash Equilibrium by fostering an environment abundant in symmetric information. This setup allows all participants to independently verify the authenticity of any portion of the Bitcoin blockchain. In the context of mathematical game theory, a Nash Equilibrium occurs when no player can benefit by changing their strategy (from honesty to dishonesty, in Bitcoin’s case), assuming all other players remain honest and neither commit nor accept fraud. This state of equilibrium is achieved by ensuring that all digital signatures and hash functions accurately match the database's records, providing a robust framework for trust where attempts at fraud become immediately apparent and easily preventable.

The resilience of this game theoretic equilibrium in the real world is underscored by the estimated 30% of all Bitcoins being irrecoverable due to lost private keys. This highlights the paramount importance of diligent key management and illustrates the Bitcoin system's inherent security; without the private key, neither the legitimate owner nor any would-be thief can access the funds. Drawing parallels with mathematical game theory, this situation mirrors the challenge of circulating counterfeit gold coins when each coin's authenticity is independently verifiable, thereby emphasizing the futility of attempting to steal Bitcoin without the private key.

Private-public key encryption is pivotal to the functionality of all Layer 1 payment processing architectures, including proof-of-work, proof-of-stake, and other blockchain consensus mechanisms. This encryption method empowers all honest participants to quickly identify and dismiss any fraudulent transactions. This essential verification and transparency principle is adeptly woven into the TNT system, substantially reducing the possibility of fraudulent payments. By providing transparent and equal access to account balances and transaction histories to all network nodes during specific periods allocated for processing current payment requests—while temporarily halting new requests—the system leverages batch processing to ensure comprehensive transparency and maintain information symmetry throughout the network. As a result, transactions proceed based on precise and universally accessible data, effectively nullifying fraud risk and markedly enhancing the network's integrity and reliability.

Bitcoin's stability and reliability are anchored in the principle of symmetric information, where equal access to transaction data for all participants establishes it as a robust store of value. This equitable information distribution is essential for maintaining the Nash Equilibrium, reinforcing the notion that honesty is the most beneficial policy for everyone involved. However, this equilibrium faces challenges from information asymmetry, especially in scenarios where traditional financial institutions' batch processing methods—employed not only by banks like JP Morgan but also by stock exchanges such as the NYSE and NASDAQ—are absent.

In the realm of cryptocurrencies, the risk of information asymmetry arises from the practice of unregulated payment requests. Unlike the structured approach of batch processing, which organizes and schedules transactions, cryptocurrencies often allow end users to initiate payment requests without such regulatory mechanisms. This leads to disparities in knowledge among peer-to-peer nodes regarding pending transactions. Often misconceived by software developers not deeply acquainted with mathematical economics as a double-spending issue, the root of this challenge is actually asymmetric information. This discrepancy highlights the importance of understanding the economic principles underlying cryptocurrency transactions and the need for mechanisms that ensure information symmetry to uphold the system's integrity and equilibrium.

From Lemons to Ledgers: Navigating Information Asymmetry in the Blockchain Era

George A. Akerlof, a Nobel Laureate in economics, illuminated how asymmetric information could encourage fraudulent behavior in any free market system. His groundbreaking analysis on the market for 'lemons,' or second-hand cars, revealed the critical importance of information symmetry in safeguarding the integrity and reliability of markets, including Bitcoin. Akerlof demonstrated how information disparities could precipitate market failure, highlighting the necessity for equitable information access among all participants to ensure transactional confidence and fairness. This concept is vitally relevant to cryptocurrencies, illustrating the need for transparent and universal access to transaction data to prevent fraud and maintain the system's integrity.

Blockchain platforms, including Bitcoin, Ethereum, and various decentralized finance (DeFi) platforms, lack a direct method to independently verify a spender's ability to fulfill payment commitments. While these systems excel at detecting unauthorized or fraudulent transactions—thus reinforcing their reputation as secure stores of value—they rely on intermediary nodes, such as miners or validators, to execute payment processing. This reliance stems from the absence of an intrinsic mechanism to ensure the availability of adequate funds for all transactions. Consequently, the need for centralized processing by these delegate nodes can diminish the effectiveness of Bitcoin and similar cryptocurrencies as mediums of exchange.

The process of transaction verification in cryptocurrencies is characterized by inefficiencies, delays, and elevated costs, highlighting its shortcomings and increasing the risk of fraud, especially in scenarios involving payment processing. Moreover, the lack of a mechanism for direct fund sufficiency verification introduces the risk of a 51% attack, a vulnerability primarily associated with the proof of work (PoW) consensus mechanism. This potential threat further accentuates the challenges faced by blockchain systems in maintaining security and reliability in transactions.

The integration of game theory principles into Bitcoin's framework has markedly contributed to its valuation and robustness. The creation of a stable Nash equilibrium within the Bitcoin network acts as a formidable barrier against fraud, rendering such attempts economically futile for potential perpetrators. Specifically, the prohibitive costs associated with conducting fraud, particularly in the context of proof-of-work (PoW) mining, have significantly fortified Bitcoin's security infrastructure and fueled its widespread adoption.

In the realm of mathematical game theory, the economic outlay of engaging in fraudulent conduct is a critical determinant of a system's integrity. For Bitcoin, the substantial expenses linked to fraud attempts—stemming largely from the resource-intensive demands of PoW mining—are economically dissuasive. These costs, encompassing electricity consumption, cooling systems, and specialized mining hardware, erect a costly barrier to malicious activities.

While alternative frameworks like proof of stake (PoS) also implement mechanisms to prevent fraud, with delegated validators overseeing payment processing, the cost barrier to fraud is typically lower than in Bitcoin. This reduced cost in alternative systems illuminates their potentially higher counterparty risk from a game theory perspective, although it's noteworthy that their associated risks may still fall below those of conventional fiat currencies managed by banks.

Consequently, Bitcoin's ability to deter fraud through the economic impracticality of attacks not only cements its position as a secure and reliable cryptocurrency but also showcases the application of game theory principles in reinforcing trust and stability within digital currencies.

Leveraging this groundwork, TNT pioneers solutions to tackle information asymmetry by incorporating batch processing. This development not only bolsters the system's robustness and security but also elevates its operational efficiency. Consequently, TNT emerges as a formidable leap forward in blockchain technology, poised to reshape the realm of digital finance profoundly. Yet, this marks merely the initial phase of its potential influence on the financial ecosystem.

Enhancing Security and Trust in Decentralized Finance: The TNT-Bank Money System

The TNT (Trust Network Technology) payment system represents a groundbreaking innovation in digital finance, employing game theory to establish a secure, decentralized financial ecosystem. By achieving Nash Equilibrium through the adoption of batch processing and a dual approval mechanism, TNT significantly enhances the integrity and security of transactions.

Batch Processing: TNT adopts a strategic approach by scheduling transactions at specific intervals, such as even minutes, and temporarily halts the acceptance of new payment instructions during these periods. This method fosters consensus among nodes about debit-credit pairs within the designated times. Through comprehensive, independent verification by all nodes, the system ensures a precise match between debits and credits, thereby eliminating the risk of any account balance becoming negative. Drawing inspiration from traditional banking practices like daytime check collection and overnight batch processing, TNT adapts this methodology for the digital era, facilitating efficient and secure transaction settlements.

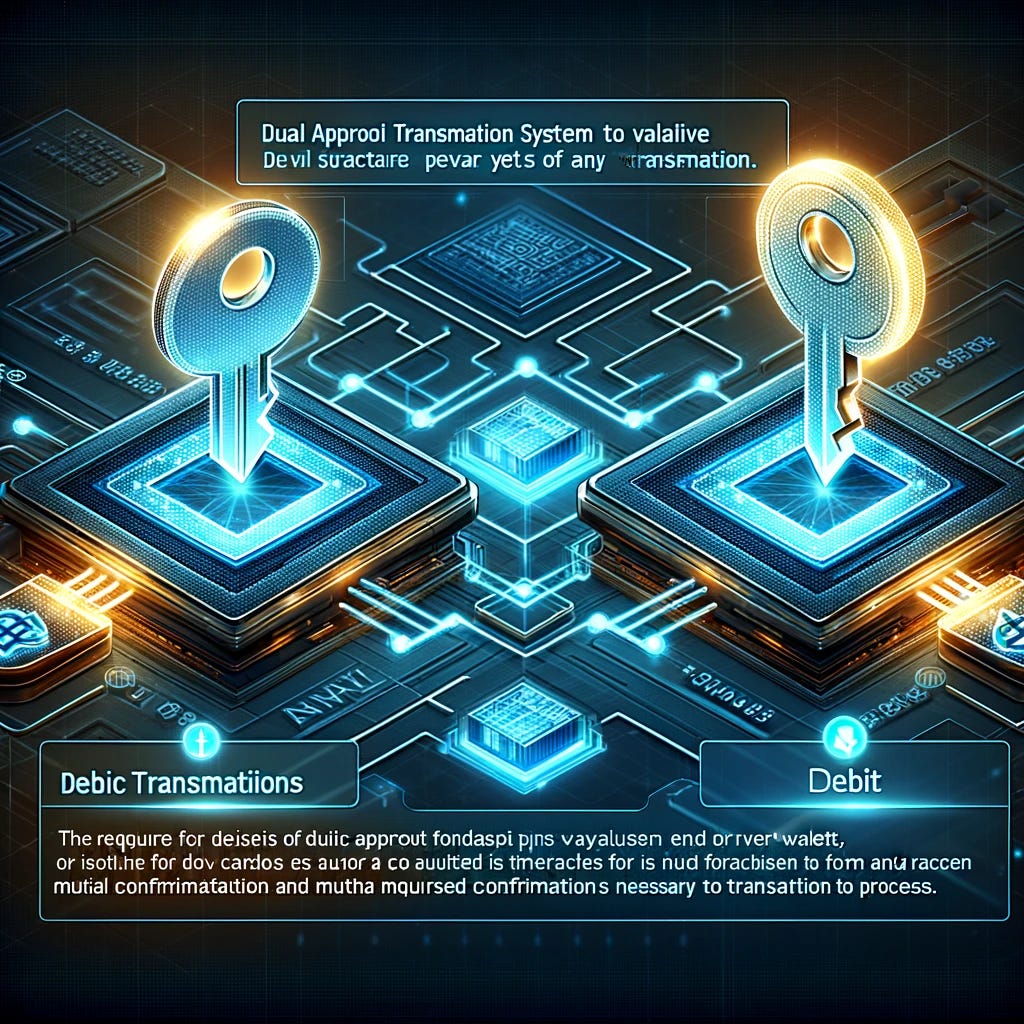

Dual Approval: To further enhance its security framework, TNT implements a rigorous dual approval process for all transactions. This protocol mandates two distinct public-private key pairs for each wallet: one set authorizes debit requests by spenders, and another set allows recipients to confirm credit transactions. The necessity of dual signatures ensures the invalidation of any transaction lacking mutual confirmation from both parties involved, safeguarding the integrity of account balances within the TNT system. Transactions failing to secure the required digital signatures, thus not aligning the spender's debit authorization with the recipient's credit confirmation, are declared invalid. This safeguard ensures that unsuccessful or unrecorded payment attempts do not compromise any account's financial status within the network. A notable benefit of this dual approval mechanism is its empowerment of credit recipients to independently verify the availability of funds in the spender's wallet before finalizing the transaction and accepting the credit. Payments not meeting these criteria are automatically nullified, effectively preventing fraudulent activities.

By requiring dual approval, TNT not only substantially improves the system's security but also cultivates a strong sense of mutual trust among participants. This method virtually eliminates the possibility of unauthorized fund transfers, thereby protecting the network against potential security breaches. As a result, this strategy ensures the safeguarding of financial assets for all network participants, underscoring the TNT payment ecosystem's reliability and security.

Through the incorporation of these innovative mechanisms, the TNT payment system demonstrates the practical application of game theory in crafting a secure, efficient, and trustworthy digital finance environment. It showcases the effective use of Nash Equilibrium in decentralized financial systems to enhance security, maintain transactional integrity, and establish a reliable network for all users.

Enhancing Security in Decentralized Finance: Leveraging Batch Processing and Game Theory

The integration of batch processing within the TNT (Trust Network Technology) system serves as a formidable barrier against fraudulent transactions. By distributing account balance information across all nodes before executing the update block, TNT effectively precludes transactions that could lead to overdrafts, ensuring their immediate rejection. This strategy forms the bedrock of TNT's security framework, utilizing game theory to foster an environment characterized by complete information symmetry. Such an environment naturally encourages voluntary, transparent trading practices among participants.

The system's intrinsic transparency and the prompt dissemination of information render any deceitful attempts instantly detectable. This universal access to information empowers the network to collectively and individually identify and mitigate fraud, particularly by the transaction's intended recipient. Recipients have the capability to independently assess and, if necessary, reject a transaction by refraining from providing their digital signature for the credit, thereby halting the flow of illegitimate funds.

This dual-layered approach to fraud detection—enabling both collective oversight and individual transaction verification—underscores the robustness of the TNT system's security measures. By necessitating independent verification and explicit consent for each transaction, TNT guarantees that only legitimate transactions are processed. This framework not only preserves the network's integrity but also grants participants complete control over their financial transactions and account balances, substantially diminishing the potential for fraud.

By synergizing batch processing with the principles of game theory, TNT establishes itself as a leader in secure digital finance. This blend of cutting-edge technological solutions and economic theory creates a secure, transparent, and fair trading environment, markedly reducing the risk of fraudulent transactions and protecting the integrity of financial exchanges. Through these innovative strategies, the TNT system embodies a holistic and proactive stance on maintaining transactional integrity and combating fraud, setting a new standard for security in the digital finance arena.

Securing Digital Assets: Game Theory in Bitcoin and TNT Systems

The Trust Network Technology (TNT) system and Bitcoin are forefront in applying game theory principles within the cryptocurrency landscape, each pioneering unique approaches to security and transaction validation. Bitcoin established the foundational role of digital signatures in verifying transaction authenticity and integrity, whereas TNT has expanded on this groundwork by integrating a dual approval process that deepens game theory's application in decentralized finance.

Digital Signatures in Bitcoin: Bitcoin ensures the security of transactions through digital signatures. Each transaction mandates a valid digital signature for network acceptance, thwarting unauthorized spending. This mechanism capitalizes on the rational behavior of nodes, which collectively reject any transaction devoid of the necessary digital signature, thus preserving network integrity.

Dual Approval in TNT: Advancing beyond Bitcoin's validation concept, the TNT system introduces a dual approval requirement for transactions. This necessitates confirmations from both the transaction initiator and the recipient, aligning with game theory principles by promoting a Nash Equilibrium of symmetric information. This augmentation of the validation process not only heightens transactional transparency and mutual consent but also strengthens cryptographic security against unauthorized digital asset usage, echoing the security benefits seen with Bitcoin's digital signatures.

The Nash Equilibrium facilitated by these mechanisms ensures transactions are transparent and mutually agreed upon, markedly reducing the possibility of unauthorized or fraudulent transactions. TNT's dual approval process, paralleling Bitcoin's digital signature prerequisite, exemplifies game theory's crucial role in protecting digital assets within a decentralized financial ecosystem.

The comparison between the substantial Bitcoins presumed permanently lost due to private key misplacement and TNT's stringent security measures underscores the practical implications of game theory in cryptocurrency security. Both scenarios highlight the indispensable value of cryptographic security and information symmetry in deterring unauthorized digital asset access.

By melding sophisticated cryptographic methods with game theory principles, the TNT system demonstrates how advanced security architecture can guarantee transactions are consensus-based and adhere to stringent security norms. This positions the theft of TNT assets as formidable as unauthorized Bitcoin transactions, showcasing game theory's efficacy in minimizing counter-party risk in decentralized finance.

Revolutionizing Digital Finance: TNT-Bank's Path to Financial Sovereignty

The Trust Network Technology (TNT) system stands at the vanguard of the digital finance revolution, leveraging the synergy of open-source software with the strategic nuances of game theory. This avant-garde methodology signals the dawn of a new era in collaborative finance, characterized by an intrinsic resistance to fraud and a substantial enhancement of financial sovereignty for its participants. Diverging from conventional financial paradigms, TNT-Bank embodies the ethos of complete disintermediation, enabling participants to independently verify transactions, thereby obviating the need for intermediary nodes.

TNT-Bank equips its users with the tools to operate their own cost-effective, AWS-hosted online nodes. This architecture utilizes transparent, open-source software that any user can compile, thereby promoting a significant level of autonomy and direct control over transaction authenticity. This framework facilitates a direct transaction flow to users' wallets, bypassing traditional financial intermediaries. Such a model of autonomy not only fortifies security but also democratizes the transaction verification process. Transactions are directly logged between the spender and recipient’s nodes and consistently replicated across the network, all underpinned by a universally trustworthy, open-source codebase.

The deliberate move towards disintermediation is critical in diminishing counterparty risk, thereby reinforcing TNT-Bank's currency as both a secure medium of exchange and a reliable store of value. These innovations elevate TNT-Bank money beyond mere enhancements in security and transactional integrity; they are redefining the contours of digital finance. By offering users unprecedented governance over their financial interactions and safeguarding their independence within the financial ecosystem, TNT-Bank is pioneering a novel paradigm for financial sovereignty in the digital epoch.

Balancing Flexibility and Security in TNT-Bank Money: A User-Centric Approach

The Trust Network Technology (TNT) system is meticulously designed to meet the varied needs and technical proficiency of its user community, showcasing a dynamic approach to transaction verification. At its heart, TNT prioritizes user empowerment, advocating for the personal oversight of nodes. This principle is carefully balanced with the recognition that not all users wish to engage deeply with the system's technical aspects. For those seeking a more streamlined experience, TNT offers access to system-endorsed, highly reliable core-primary nodes. These critical nodes are democratically elected by the user community, ensuring the node selection process for payment verification is transparent and founded on mutual trust.

This dual-path strategy grants users the liberty to choose from a spectrum of reputable nodes, enabling seamless integration with wallet applications for efficient payment processing. Such versatility ensures that TNT-Bank money maintains the user-friendly and accessible qualities characteristic of leading cryptocurrencies. It permits users to entrust their transactions to a reliable peer-to-peer node, mirroring widespread practices within the cryptocurrency sector. For instance, many Bitcoin users opt not to run their nodes, instead connecting their wallets to a trusted, well-established node. These intermediary nodes are instrumental in transmitting payment requests to miners and verifying coin balances against the blockchain's most current version. In a similar vein, TNT-Bank's trusted nodes render TNT-Bank money as user-friendly and straightforward as traditional cryptocurrencies, catering to users with varying degrees of technical involvement and participation.

The integration of system-supported, reliable nodes offers a pioneering solution in digital banking, particularly appealing to those who value simplicity. This innovative feature allows bank clients to effortlessly provide the payment recipient's dual-approval secondary key to their system-designated incoming payment approval node. Crucially, the primary key, essential for authorizing transactions, remains securely stored within their private wallet application. This dual-key architecture is a testament to TNT's dedication to forging a secure, efficient, and user-centric digital finance ecosystem. It exemplifies how TNT is navigating the complexities of the decentralized finance space by providing a service that balances ease of use with rigorous security measures. As such, TNT positions itself as an attractive option for users seeking both the autonomy of decentralized finance and the convenience of traditional banking systems.

By melding the independence of self-verification with the ease of centralized, credible nodes, TNT-Bank money offers a hybrid model that caters to the diverse preferences of its users. This balanced approach makes the benefits of secure, decentralized finance accessible to a broad audience, reflecting TNT's vision for a digital financial future that prioritizes security, efficiency, and user friendliness for all participants.

Redefining Efficiency in Digital Finance: TNT-Bank's Integration of Smart Contracts and Rapid Transactions

The Trust Network Technology (TNT) system ushers in a new era for digital finance, combining the versatility of Smart Contracts with transaction speeds that challenge those of leading financial networks like FedNow and Visa. This fusion is a testament to TNT's dedication to pushing the boundaries of efficiency and cost-effectiveness, thereby establishing a new benchmark for transaction processing in the industry.

TNT-bank money sets an ambitious target: a 6-second guaranteed processing time, made possible by an innovative approach to batch processing transactions at 3-second intervals. This level of efficiency is not only achievable with today's technology, which features ubiquitous internet access and the widespread availability of precise online atomic clocks, but it also significantly enhances the user experience by drastically shortening transaction wait times. Furthermore, TNT's model emerges as an environmentally friendly alternative to the energy-intensive mining operations associated with many current cryptocurrencies. Remarkably, a TNT bank payment requires minimal CPU usage, limited to the verification of digital signatures—a task that demands merely a fraction of the computational power traditionally required. Apart from the need for synchronized clocks, no additional CPU resources are expended.

Through this strategic innovation, TNT demonstrates its capability to not only significantly boost transaction efficiency but also to affirm its commitment to environmental sustainability. With the incorporation of these advanced features, TNT-bank money is set to transform the standards of digital transactions, offering a secure, rapid, and eco-conscious choice for users exploring alternatives to conventional cryptocurrency mechanisms.

Revolutionizing Digital Agreements: TNT-Bank Money's Integration of Smart Contracts

The incorporation of Smart Contracts into the Trust Network Technology (TNT) ecosystem signifies a monumental leap forward in digital finance. By codifying the terms of agreements, which can then be independently verified via digital signatures by all parties involved, TNT ushers in an unprecedented era of trustlessness in financial transactions. These contracts are executed by open-source software, compiled independently and seamlessly integrated across the network of honest TNT bank nodes, broadening the scope of TNT's smart contract applications. This architecture enables a wide array of financial activities, from straightforward transfers to intricate, conditional operations, all within TNT's secure and decentralized framework.

Smart Contracts within TNT-bank money redefine how agreements are executed and verified. By ensuring that contracts are activated at specific future batch processing times and providing accurate execution records, TNT facilitates transparent scheduling for both the initiation and conclusion of contracts. This precision opens up new avenues for Smart Contracts, establishing TNT-bank money as a premier platform for diverse financial agreements and transactions.

The implementation of Smart Contracts in the TNT framework stands out for its cost-effectiveness, marking it as an economically attractive choice in the realm of digital finance. This cost-efficiency is supported by a robust architecture of verifiable integrity, reinforced by a Nash Equilibrium that effectively neutralizes any potential for deceit or fraud. As a result, every Smart Contract on the TNT platform is not only executed without fees but also guaranteed to be secure and invulnerable to tampering.

By weaving Smart Contracts into its fabric, TNT-bank money positions itself at the forefront of digital financial innovation, offering a secure, streamlined, and adaptable mechanism for automating and overseeing contractual agreements. Leveraging blockchain technology and game theory, TNT-bank money's Smart Contracts provide a dependable and fraud-resistant framework for executing a wide variety of financial transactions. This advancement not only extends the functionalities of TNT-bank money but also sets a new benchmark for digital contract execution, exemplifying unparalleled reliability, security, and cost-efficiency.

Leading the Charge in Digital Finance: The Revolutionary Impact of TNT-Bank Money

The integration of high-speed transaction processing with advanced Smart Contracts propels TNT-bank money to a leadership position in the digital finance landscape. This pioneering system breaks new ground beyond conventional payment methods, offering a solution that is swift, environmentally friendly, and highly versatile, catering to the evolving demands of the modern financial sector.

With its commitment to efficiency, security, and environmental responsibility, TNT-bank money is forging a visionary path for the future of finance. This approach not only boosts operational efficiency but also broadens the spectrum of financial services available, advocating for a financial ecosystem that is inclusive and sustainable. Transactions within this system are characterized by their rapid execution and robust security, guaranteeing that financial services are reliable and universally accessible.

Exploring the essence of TNT-bank money reveals its potential to significantly alter the financial landscape. Distinguished by unmatched security and operational efficiency, TNT-bank money utilizes game theory principles to minimize fraud and enhance trust in a decentralized environment.

For those interested in a deeper exploration of TNT-bank money's innovative features and its impact on the future of finance, a visit to tnt.money provides an exhaustive resource. The site delves into the groundbreaking contributions of Trust Network Technology in redefining commercial transactions and setting new standards for financial security, showcasing how TNT-bank money is redefining benchmarks in digital finance.